Topic hub

Money, Business & Personal Growth

Open the wider hub for connected guides, references, questions, and works.

Explore topicMoney isn’t just numbers—it can influence your wellbeing, decisions, and day-to-day peace of mind.

Money matters because it buys options and reduces uncertainty. When you have a buffer, you can make calmer choices, plan ahead, and recover from setbacks faster. When you don’t, stress and short-term thinking often take over, shaping your financial habits and even your relationships. The goal isn’t to chase status—it’s to create financial security that supports how you want to live.

Start with the section that matches your intent now, then return to the full article when you want the complete picture.

Open the wider hub for connected guides, references, questions, and works.

Explore topicMoney isn’t just a topic for spreadsheets or career conversations—it quietly affects how safe you feel, what you choose to do next, and how much stress you carry. If you’ve ever wondered why money seems to matter so much in your decisions, you’re not alone. Understanding why money matters can help you build personal finance habits that support your wellbeing, not fight against it.

Money matters because it reduces uncertainty and expands your options. When you have a little financial security, you can make choices with less fear and fewer compromises. When you don’t, your brain treats finances like an ongoing threat, which often leads to avoidance, rushed decisions, and stress-driven financial habits.

What money really buys you: security and choice

Money buys stability first, not luxury. Think about the difference between “I’ll figure it out” and “I have a plan.” A small emergency buffer, predictable bill coverage, and a realistic budget can turn a potential crisis into a manageable problem. That’s what financial security looks like in day-to-day life.

It also buys choice. Budgeting isn’t about depriving yourself; it’s about deciding what your money is for. When your plan matches your values—health, family time, learning, travel, or simply less chaos—you’re less likely to feel stuck. Without a plan, every decision becomes urgent, and you end up spending to solve feelings rather than needs.

Your money mindset is the lens you use to interpret financial events. If you grew up with scarcity, you might assume money is always unstable. If you’ve had setbacks, you may expect things to go wrong. These beliefs can be protective, but they can also steer you toward habits that keep you stressed.

For example, when you believe you can’t catch up, it’s common to avoid budgeting because seeing the gap feels painful. Or you might overspend right after doing “hard thinking,” because relief feels like reward. None of this means you’re failing—it means your system is responding to stress.

Money stress isn’t only emotional; it changes how you behave. Under uncertainty, people often default to short-term coping. That might look like using credit to delay discomfort, buying convenience items to reduce tension, or skipping the planning step because it feels like too much work.

Over time, you can get a loop: worry leads to avoidance, avoidance delays clarity, and delayed clarity increases worry. Breaking the loop usually isn’t about willpower. It’s about building a simpler process—one that creates clarity quickly and reduces the number of decisions you have to make while anxious.

Money matters becomes obvious in patterns. You might feel anxious when bills arrive, delay checking your balance, or experience decision fatigue around everyday purchases. You may start saving, then stop when something unexpected happens—often because the plan didn’t include a buffer.

In relationships, money can show up as tension or silence. One person may want to talk budgets; the other may avoid the topic. Disagreements can feel personal, but they’re often about different levels of security and different expectations about responsibility.

And if you notice shame—“I should be better at this”—pause. Shame increases avoidance. Curiosity increases action. The goal is to understand what your money habits are protecting you from, then build a steadier plan that doesn’t require you to push through fear alone.

Financial security changes more than your account balance. It can change your confidence and your ability to focus. When your mind is occupied by “What if we can’t cover this?” it’s harder to concentrate at work, keep healthy routines, or make thoughtful decisions.

Money stress can also strain relationships. It can lead to conflict over spending priorities, resentment about who handles bills, or fear of discussing money openly. Even when you care deeply, stress can make communication sharper and less patient.

There’s also a subtle effect on motivation. If money feels like a constant barrier, opportunities can look risky or out of reach. You may stay in a job you dislike, avoid education or career moves, or hesitate to take on new responsibilities. Money doesn’t control your life, but it can remove the runway you need to pursue what matters.

Start with the smallest step that creates clarity. Make a simple monthly snapshot: income, essentials, and minimum debt payments. Keep it practical and judgment-free. If the full picture feels too big, begin with just the essentials.

Next, pick one stabilizing habit. Many people do best with a small automatic transfer into saving, even if it’s modest. The point isn’t to “fix everything.” It’s to build saving habits that show your brain progress is possible.

Then, add buffer thinking. Emergencies happen, so your plan should anticipate them. If you can’t build a full emergency fund yet, aim for a starter amount that prevents the most stressful outcomes—like relying on credit for every surprise.

Reduce friction with simple rules. A weekly 10-minute review, a spending cap for non-essentials, or a short waiting period for larger purchases can help you avoid stress-driven spending.

Finally, be kind with your money mindset. Instead of “I’m bad with money,” try “What system would make this easier?” If money stress is affecting your mental health or causing frequent conflict, consider reaching out to a qualified professional for support. A therapist can help with anxiety and shame; a financial counselor can help you design a plan you can actually maintain.

Money matters because it shapes how safe you feel and how freely you can choose. When you treat it as a tool for stability—rather than a measure of your worth—your financial habits can become steadier, and your stress can start to shrink.

Use these two paths when you want the clearest immediate continuation—one for deeper guidance, one for the broader topic map.

Learn how to find legitimate free grant money for bills and personal use. Follow a safe…

Read nextExplore the broader topic hub for connected guides, references, questions, and works.

Explore topicMost readers do not get stuck because the topic is too complex. They get stuck because they assume one herb, one dose, or one quick answer should solve every situation. In reality, the strongest results usually come from matching the right remedy to the right context and using it with consistency.

When you want broader context around this answer, use these connected pages to expand your understanding across the full cluster.

Learn how to find legitimate free grant money for bills and personal use. Follow a safe…

Read next

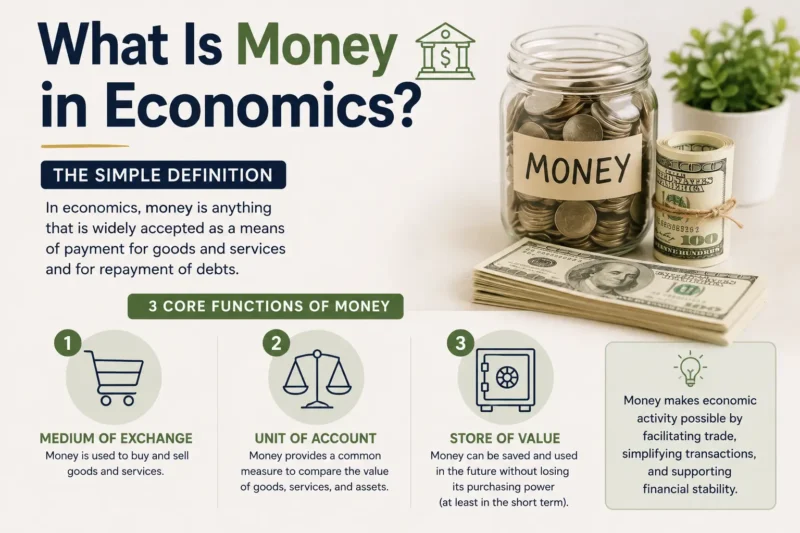

Money in economics is more than cash. It’s a system used to make trade easier through…

Read next

Explore 15 definition of money perspectives, from economics to daily life. Learn what every definition agrees…

Open reference

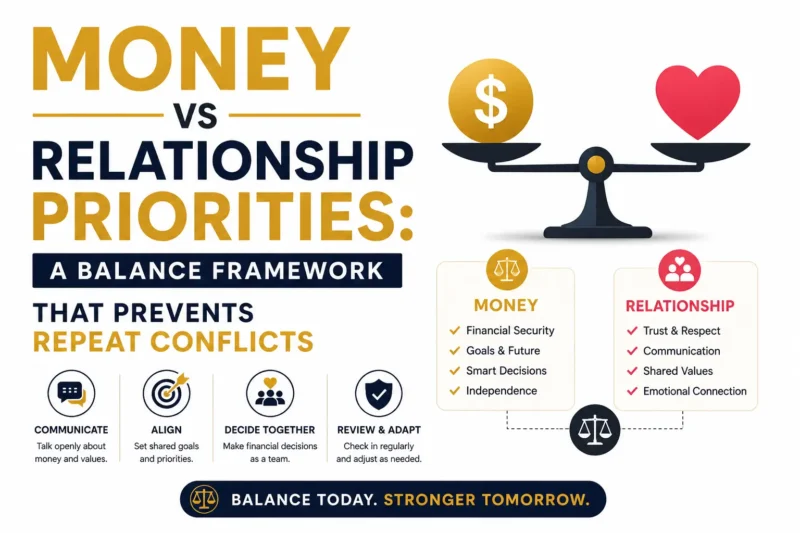

Compare money vs relationship priorities with a clear alignment framework. Learn how to balance values, communication,…

Compare nowYes. Money matters because it affects how secure you feel, not just how much you earn. Even modest savings, predictable bill coverage, and a basic budget can reduce uncertainty. That lowers stress and makes it easier to plan ahead. You don’t need wealth to get benefits—you need enough stability to handle surprises and make decisions with less fear.

Money stress often comes from uncertainty: not knowing if bills will be covered, how debt will change, or what emergencies might cost. When your brain treats finances as a recurring threat, it can lead to avoidance, constant checking, and decision fatigue. Over time, stress-driven financial habits can reinforce the cycle. Creating clarity and a small buffer can reduce that mental load.

Budgeting is how you turn money from a source of anxiety into a tool for choice. A budget clarifies what’s required each month and what’s flexible, so you can spend intentionally instead of reacting. It also supports saving because you can see how much room you truly have. Done well, budgeting reduces guilt and increases control.

When money is tight, your options shrink and your brain shifts toward short-term coping. That can look like delaying bills, relying on credit, or spending impulsively to feel better now. Avoidance also becomes common because looking at the full picture feels overwhelming. These behaviors reduce discomfort in the moment, but they usually increase stress later—so a simpler, steadier plan helps break the loop.

Often, yes. A money mindset improves when your environment and process change—like building a small saving habit, tracking essentials, and creating rules for spending. These actions provide evidence that you can handle financial reality, which reduces shame and helplessness. Increasing income can help, but stability and clarity can move your mindset even before your paycheck changes.

Consider professional help if money anxiety is persistent, affecting sleep or relationships, or if you’re stuck in cycles like compulsive spending, chronic avoidance, or unmanageable debt stress. A financial counselor can help you design practical next steps, while a therapist can support anxiety, shame, and conflict patterns. Getting support early can prevent stress from becoming harder to unwind.

Money matters most when it’s tied to uncertainty. The moment you replace guesswork with a simple plan—clear essentials, a small saving habit, and a bit of buffer—you give your mind permission to relax. That doesn’t mean ignoring bigger goals or pretending everything is fine. It means building financial security step by step, so your choices come from your values instead of your anxiety.