Topic hub

Money, Business & Personal Growth

Open the wider hub for connected guides, references, questions, and works.

Explore topicA clear economics definition of money, plus the functions it serves in everyday life.

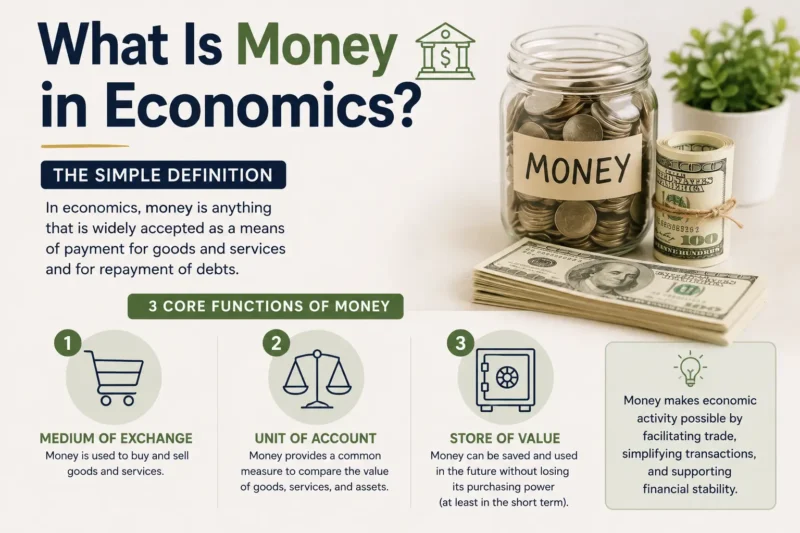

In economics, money is anything widely accepted as payment for goods and services. It helps people compare prices (unit of account), trade without direct barter (medium of exchange), and hold purchasing power over time (store of value). When money performs these functions well, transactions become faster, cheaper, and easier for households and businesses.

Start with the section that matches your intent now, then return to the full article when you want the complete picture.

Open the wider hub for connected guides, references, questions, and works.

Explore topicMoney is one of those words people use every day, but economists use it in a more specific way to explain how economies actually work. In everyday terms, money helps you buy things and pay bills; in economics, it’s defined by the roles it plays in exchange. Understanding what money is in economics can make budgeting, saving, and even business decisions feel clearer.

Money in economics is anything that’s widely accepted as payment for goods and services. The definition isn’t only about whether it’s a coin or a banknote. It’s about whether people treat it as a reliable way to settle transactions. If most sellers accept it, and buyers can use it later, it functions as money.

Economists also emphasize that money is a “system,” not just an object. That system includes trust, rules, and payment infrastructure. When those pieces are stable, money becomes easier to use for daily exchange. When they’re not, money’s ability to coordinate trade can weaken.

A helpful way to remember money is to focus on its functions. Economists often summarize them as a medium of exchange, a unit of account, and a store of value.

Medium of exchange: This is what lets you trade without barter. You sell or earn value, then use money to buy what you need.

Unit of account: This is the measuring stick for prices, wages, and debts. When everything is quoted in the same currency, it’s easier to compare options and plan.

Store of value: This is how money can be held for later spending. If money holds purchasing power reasonably well, people are more willing to save it.

These functions reinforce each other. If money is accepted and easy to use, it becomes a stronger medium of exchange. If prices are stable enough, it becomes a better unit of account and a more trustworthy store of value.

A common confusion is mixing up money with wealth. Wealth includes assets you own that have value, such as a home, shares, a business, or collectibles. Money is a specific way that value can be held and used for transactions.

You can be “wealthy” but short on money if most of your value is tied up in assets you can’t quickly spend. You can also have money but not much wealth if you’re living on income without meaningful assets.

This distinction matters because it changes the advice you need. If you’re cash-poor but asset-rich, your challenge might be liquidity and timing. If you’re money-rich but asset-poor, your focus might be saving and building long-term value. Money’s economic functions are the bridge between these realities.

Types of money in economics (and why it’s not only cash)

When people hear “money,” they often think of physical cash. In economics, “types of money” can include several forms that serve similar roles.

This is money with intrinsic value—something that can be used for purposes other than payment. Historically, certain metals were used this way. The downside is that commodity money can be expensive to store and may be harder to manage consistently.

Representative money is backed by a claim on another asset. For example, older systems used notes that could be exchanged for something of value. The point is that the note’s value comes from the promise behind it.

Fiat money has value because the government and the public use it for payment. Coins and banknotes are the common examples. Fiat money works when people trust the system and when institutions support stable pricing and payment.

In modern economies, money often exists as bank balances. You might not hold cash, but you can transfer deposit money electronically. For most practical purposes, deposits can function as money because they are widely accepted for payment.

A useful boundary: “money” can mean different things depending on what an economist is measuring. Some definitions focus on what people use for payment; others use broader categories to track liquidity in the economy. If you’re reading research or news, pay attention to the definition used.

Money is most useful when all three functions work well. In real life, they can weaken—sometimes gradually, sometimes quickly.

If inflation rises, money’s store-of-value function can deteriorate. People may spend faster or look for alternatives that better preserve purchasing power.

If trust drops, money may become less accepted. Sellers might demand payment in different forms, or contracts may become harder to denominate.

If payment systems fail, money’s medium-of-exchange role becomes less reliable. Even a stable currency can feel unstable if transfers are delayed or costly.

These changes don’t happen in a vacuum. They often connect to expectations about the future, the credibility of institutions, and the stability of economic policy. That’s why economists watch not just prices today, but also what people expect prices to do tomorrow.

You can see money’s functions in small moments.

When you check your paycheck and see it in a currency amount, that’s a unit of account in action.

When you pay for groceries with a card or a transfer, that’s a medium of exchange.

When you set aside savings for rent next month, that’s a store of value—though the “quality” of that function depends on inflation and interest.

Even your debt payments reflect money’s functions. Loans are measured in the unit of account, and repayment relies on money being a dependable medium of exchange. If the currency loses stability, the real burden of fixed debt can change significantly.

Money and personal growth: a practical mindset

Understanding money in economics can help with personal growth because it reframes money from “a number” to a tool with specific jobs. When you treat money as a tool, you tend to ask better questions.

Instead of only asking, “Do I have enough money?” you also ask, “Is my money stable enough to plan with?” and “Am I using it in ways that match my time horizon?”

For example, it’s reasonable to keep emergency funds in accessible accounts because you need the medium-of-exchange function. For longer-term goals, you may consider options that aim to preserve value better than cash alone, because you’re relying more on the store-of-value function.

This doesn’t require perfect predictions. It just requires matching your strategy to what the function needs to do for you.

You’ll hear many “money rules” online, but not all of them are talking about the same thing. Some advice focuses on saving, which relates to a store of value. Other advice focuses on budgeting and pricing, which relates to units of account. Other advice focuses on payment timing and liquidity, which relates to the medium of exchange.

Before you follow a recommendation, check what function it’s really addressing. If someone tells you to “just hold cash,” they’re implicitly betting that cash will remain a good store of value. If someone tells you to “avoid cash entirely,” they may be ignoring how useful cash or deposits are for medium-of-exchange needs.

A balanced approach is usually best: keep enough liquidity for your obligations, and choose longer-term strategies that fit your risk tolerance and time horizon.

Use these two paths when you want the clearest immediate continuation—one for deeper guidance, one for the broader topic map.

Want better money habits without overwhelm? Try this simple 7–30 day system: track spending, set goals,…

Read nextExplore the broader topic hub for connected guides, references, questions, and works.

Explore topicMost readers do not get stuck because the topic is too complex. They get stuck because they assume one herb, one dose, or one quick answer should solve every situation. In reality, the strongest results usually come from matching the right remedy to the right context and using it with consistency.

When you want broader context around this answer, use these connected pages to expand your understanding across the full cluster.

Want better money habits without overwhelm? Try this simple 7–30 day system: track spending, set goals,…

Read next

Money shapes your daily choices, stress level, and sense of security. Here’s why it matters, what…

Read next

Explore 15 definition of money perspectives, from economics to daily life. Learn what every definition agrees…

Open reference

Compare money vs relationship priorities with a clear alignment framework. Learn how to balance values, communication,…

Compare nowIn economics, money is defined by what it does—especially whether it’s widely accepted for payment. That means bank deposits and electronic balances can count as money because people can use them to settle purchases. Cash is only one form. The key is acceptance and reliability in transactions, not the physical shape of the money.

Economists typically describe three core functions: money as a medium of exchange (used to buy and pay), a unit of account (used to set prices and measure value), and a store of value (held for future spending). These functions work together to reduce friction in trade and make planning easier for households and businesses.

A store of value lets people save purchasing power for later instead of having to barter immediately. If money loses value quickly—often due to high inflation—people may spend faster or look for alternatives. That can disrupt budgeting, contracts, and long-term planning, because savings become less predictable.

Unit of account means prices, wages, and debts are expressed in a common measure, usually a currency. In daily life, it’s why you can compare the cost of groceries from one store to another and why your rent and bills are easy to track. Without a shared unit, comparing options becomes confusing and costly.

When money becomes less trusted or less stable, its functions can weaken. For example, higher inflation can reduce its store-of-value role, leading people to shorten savings time. Payment disruptions can weaken its medium-of-exchange function. In extreme cases, people may demand different forms of payment or avoid long-term contracts.

Wealth includes everything you own that has value, like a home, investments, or a business. Money is a specific form of value that’s used for exchange and measurement. You can have wealth but little money if your assets are hard to sell quickly, or you can have money without much wealth if you’re not building assets over time.

Money in economics isn’t just cash in a wallet—it’s a trusted system for exchange, measurement, and saving. When you understand those functions, you can make better decisions about budgeting, payment timing, and where to store your money based on your goals. If your situation feels unstable, focus on what the functions mean for you right now: can you pay when needed, can you plan with a reliable measure, and can your savings preserve purchasing power over time?