Topic hub

Money, Business & Personal Growth

Open the wider hub for connected guides, references, questions, and works.

Explore topicMoney isn’t just numbers—it affects your daily decisions, stress, and future options.

Money matters in everyday life because it changes what you can do right now and how safe you feel. It covers essentials like housing, food, and transportation, and it also affects your choices around health, relationships, and opportunities. When money is tight, everyday decisions can become stressful and short-term. When it’s stable, you can plan, recover from setbacks, and move toward goals.

Start with the section that matches your intent now, then return to the full article when you want the complete picture.

Open the wider hub for connected guides, references, questions, and works.

Explore topicMoney isn’t just something you think about when you’re buying things. It’s part of how your day works—how safe you feel, what choices you can make, and how quickly you can recover when life gets messy. That’s why money is often emotionally loud, even when you’re not trying to think about it. If you’re searching for practical reasons behind the pressure, this page will help you connect the dots.

Money matters in everyday life because it functions like a practical tool that supports stability and choice. In real life, it shows up as the ability to cover essentials—housing, food, transportation, utilities, and basic healthcare—without constant panic. It also helps you plan ahead, so you’re not always reacting to the next surprise.

When people talk about the functions of money, they’re pointing to how money makes everyday life easier to manage. It provides a shared way to pay for needed services, compare options, and reduce the chaos of “figuring it out” every time something comes up. Money also supports independence: it can give you room to say no to harmful situations, take care of your health, or move toward opportunities that improve your future.

Just as important, money affects your mental bandwidth. If you can see where your money is going and you have a buffer, you’re more likely to feel calm and capable. When you can’t, uncertainty can turn into chronic stress. That stress can quietly affect sleep, focus, and how you handle conflict.

In other words, money doesn’t equal worth or happiness. But it can change the conditions that make those things easier to reach.

A lot of people assume the question is only about buying. But the deeper issue is usually stability and decision-making. For example, you might not be trying to “keep up with the Joneses.” You might just be trying to avoid late fees, keep your job by having reliable transportation, or afford groceries that don’t leave you short by the end of the week.

Another common confusion is that money problems automatically mean someone is “bad with money.” Sometimes it’s true—spending habits matter. But sometimes the real driver is timing (uneven paychecks), rising costs, unexpected events, or debt that makes normal life harder. When people label it as personal failure, they often miss the system problem.

Finally, people sometimes treat money like a moral scoreboard. It’s not. Money is a tool. The goal isn’t to become obsessed with it; it’s to use it more skillfully so it stops running your daily life.

The reasons it happens: how money shapes your everyday life

Money matters because it changes what’s possible right now. Essentials cost money, and essentials don’t pause. If income doesn’t cover them, you feel pressure immediately.

Cash flow is a big part of this. Even if your income is “enough” on average, the timing can create trouble. A rent increase, a car repair, or a gap between paydays can turn a manageable month into a stressful one. When bills pile up, you may start making reactive choices—paying the loudest bill first, postponing the rest, and leaning on credit when savings aren’t available.

Money also acts as a risk buffer. Emergencies happen: illness, job changes, family needs. When you have reserves, these events are painful but survivable. When you don’t, they can snowball into bigger problems.

There’s also the mental side. Scarcity can narrow your focus and increase decision fatigue. If you’re constantly recalculating how to cover the next expense, it becomes harder to think long-term. That can affect everything from your work performance to how you show up in relationships.

Finally, money influences growth. Learning skills, improving your job prospects, or starting something new often requires time and sometimes upfront costs. Without the capacity to fund growth, your options shrink.

Money matters most when you start seeing patterns in your daily routine. You might feel tense when you check your bank account, avoid opening mail, or feel your heart race when a bill arrives. You may find yourself ignoring long-term plans because you’re focused on what’s due this week.

You might also notice “patchwork” behavior: relying on credit to cover gaps, using overdrafts, switching payment plans repeatedly, or delaying repairs because you’re trying to conserve cash. Another sign is not knowing your monthly spending clearly—if you can’t explain where your money goes, it’s harder to improve money in a realistic way.

Money can also show up in relationships. Arguments may flare around fairness, spending, saving, or debt. Even when both people care, stress can make conversations sharper and less productive.

In some cases, the signs are quieter: missing doctor visits, postponing dental care, or skipping opportunities because the upfront cost feels too risky. If you’ve been making “survival” choices more often than “preference” choices, that’s a strong signal that money is affecting your decision space.

Money affects you in practical and emotional ways.

Practically, it shapes your daily options. When your budget covers basics, you can plan meals, keep appointments, and maintain reliable transportation. When it doesn’t, everyday life becomes a series of trade-offs—between groceries and health, repairs and rent, or short-term relief and long-term stability.

Emotionally, money influences stress levels and confidence. Stability supports calm, and uncertainty often triggers constant worry. That worry can drain energy you’d otherwise use for work, learning, or relationships.

Money also affects your sense of freedom. Even modest stability can create breathing room: handling a surprise expense without panic, taking a sick day without fear, or supporting someone else without ruining your own finances.

In relationships, money can be either a stress amplifier or a teamwork opportunity. When people communicate openly and agree on priorities, money becomes less of a battleground and more of a shared plan. When communication breaks down, small disagreements can turn into bigger resentments.

Finally, money affects growth. If you can’t invest in skills or tools, progress slows. When you can, you can move from survival mode to improvement mode—and that shift changes your whole trajectory.

What to do next if money feels like a constant pressure

If your goal is to improve money, start with steps that reduce stress and increase clarity. Don’t try to overhaul everything at once.

First, get clear on basics. Track your income and essential expenses for one month. Focus on categories that actually drive your life: housing, food, transportation, debt payments, childcare, and healthcare. This isn’t about blame—it’s about visibility.

Second, build a minimum stability plan. Choose one small target you can sustain, such as paying one bill on time consistently, building a tiny emergency buffer, or reducing one recurring expense. Small wins help your nervous system settle and help your finances become more predictable.

Third, reduce friction. If you’re overwhelmed, automate reminders and payments where you can. Set weekly check-ins. Keep it simple enough that you’ll actually do it.

Fourth, stop high-cost leakage. Look for fees, unused subscriptions, and interest charges that quietly drain you. Cutting one or two costly items can free up cash faster than trying to perfect your entire budget.

Fifth, consider income options with realistic expectations. If you’re exploring ways to earn money free or make extra income, be careful with scams and avoid anything that promises instant results without effort. Time, effort, and taxes still matter.

Sixth, if bills are the problem, explore legitimate help. Some people find free grant money for bills and personal use through reputable nonprofit programs and local or government-supported assistance. Avoid any program that asks for upfront payment. Verify details before sharing sensitive information.

If you want one practical next step today, choose either: track your essentials for 30 days, or pick one bill to stabilize first. When money stops being a mystery, your choices get calmer and more effective.

Money matters in everyday life because it changes how safe and flexible you feel—and that affects your choices, not just your purchases. If you’re dealing with pressure, you don’t need to “fix everything” overnight. You need clarity, one stable action, and a plan you can actually follow.

When you treat money like a system you can improve, you move from constant reaction to steady progress. And that’s when life starts to feel more like yours again.

Use these two paths when you want the clearest immediate continuation—one for deeper guidance, one for the broader topic map.

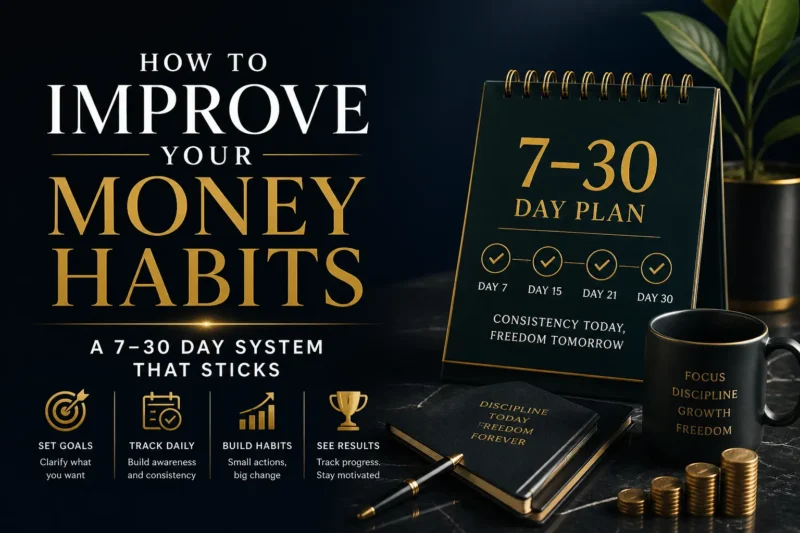

Want better money habits without overwhelm? Try this simple 7–30 day system: track spending, set goals,…

Read nextExplore the broader topic hub for connected guides, references, questions, and works.

Explore topicMost readers do not get stuck because the topic is too complex. They get stuck because they assume one herb, one dose, or one quick answer should solve every situation. In reality, the strongest results usually come from matching the right remedy to the right context and using it with consistency.

When you want broader context around this answer, use these connected pages to expand your understanding across the full cluster.

Want better money habits without overwhelm? Try this simple 7–30 day system: track spending, set goals,…

Read next

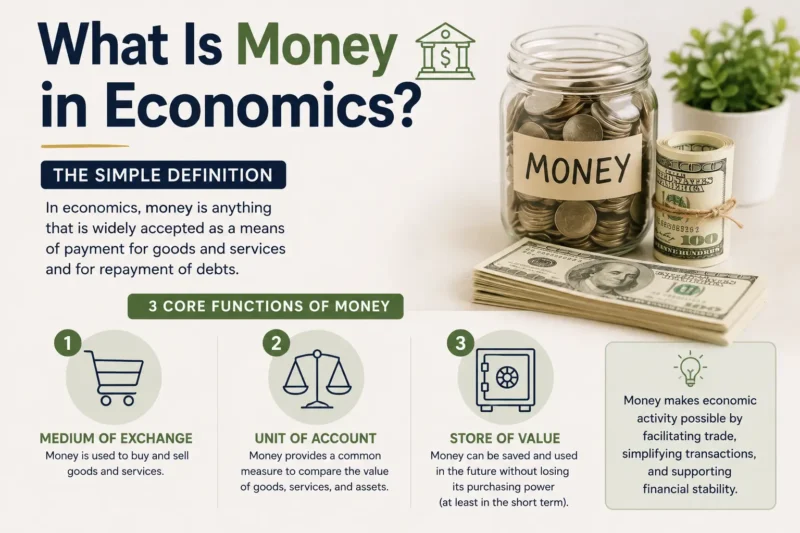

Money in economics is more than cash. It’s a system used to make trade easier through…

Read next

Explore 15 definition of money perspectives, from economics to daily life. Learn what every definition agrees…

Open reference

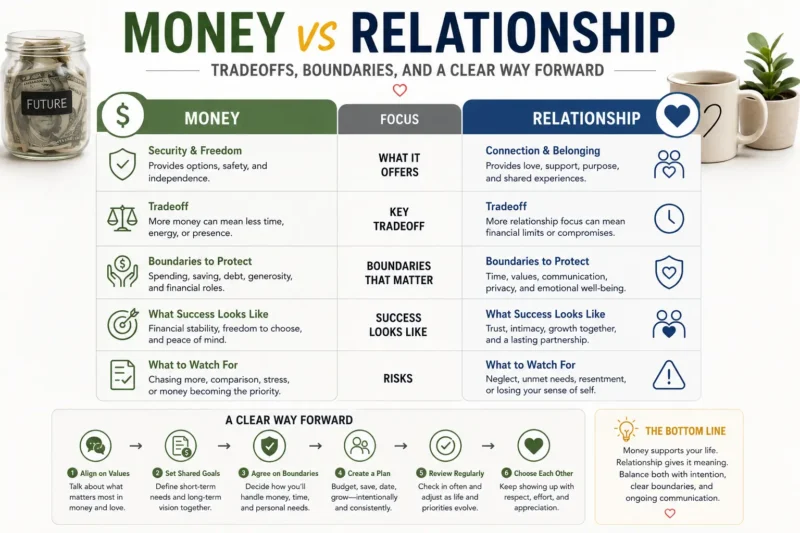

Money vs relationship isn’t a zero-sum choice. Compare the real tradeoffs, spot the conflict triggers, and…

Compare nowYes, because money influences essentials, timing, and risk. Even if someone isn’t spending much, bills, transportation, healthcare, and emergencies still require cash. When money is unpredictable, stress rises and decision-making gets narrower. When money is stable, people can plan, recover from setbacks, and focus more energy on work, relationships, and goals.

In everyday life, money helps you pay for necessities, compare options, and manage value over time. It also acts as a buffer for emergencies and supports independence—like being able to handle repairs or take time off when needed. Without money performing these roles, life becomes more reactive and harder to plan.

Start with clarity and stability, not perfection. Track essential expenses for one month, then pick one realistic target: pay one bill on time consistently, reduce one recurring cost, or build a small emergency buffer. If you can, reduce high-cost leakage like fees or interest. If you’re overwhelmed, simplify your system until it’s sustainable.

Some are legitimate, but you must verify. Look for reputable nonprofit organizations, local services, or government-supported programs. Avoid any service that charges upfront fees for access to help. If you’re unsure, check the organization’s website, contact details, and eligibility requirements before sharing personal information.

“Earn money free” typically refers to side income ideas that don’t require paying to start. Even then, you still invest time and effort, and you may owe taxes depending on where you live. Be cautious with schemes that promise quick money with little work. If it sounds too easy, it often is.

Because they often show outcomes without showing context like debt, savings, job stability, or family responsibilities. Comparing your behind-the-scenes reality to someone else’s highlight reel can increase stress and reduce motivation. If you notice that effect, limit exposure, focus on your own numbers, and set small goals you can control.

Money matters in everyday life because it changes how safe and flexible you feel—and that affects your choices, not just your purchases. If you’re dealing with pressure, you don’t need to “fix everything” overnight. You need clarity, one stable action, and a plan you can actually follow. When you treat money like a system you can improve, you move from constant reaction to steady progress, and life starts to feel more like yours again.