Topic hub

Money, Business & Personal Growth

Open the wider hub for connected guides, references, questions, and works.

Explore topicMoney is a system-wide tool economists use to explain how trade, pricing, and value storage work.

In economics, what is money in economics? Money is a widely accepted medium of exchange. It lets buyers and sellers trade without needing a direct barter deal, helps everyone quote prices using a shared unit of account, and can preserve value as a store of value—though inflation can reduce that value over time.

Start with the section that matches your intent now, then return to the full article when you want the complete picture.

Open the wider hub for connected guides, references, questions, and works.

Explore topicMoney is one of those words people use every day, but economics treats it as a specific system that helps society trade efficiently. When you understand what money is in economics, the everyday “why does this matter?” questions—like budgeting, inflation, and pricing—become easier to see. Let’s break it down clearly, starting with the direct definition and then moving into money’s core jobs.

In economics, money is broadly accepted as payment. It’s something people can use to settle transactions for goods and services, and it’s recognized as a common standard for measuring value. That “broad acceptance” is the key idea: money isn’t just an object; it’s a role in the economy.

Economists usually describe money through functions rather than a single property. A thing counts as money when it reliably serves those functions for most people in a given economy. For example, bank deposits are often treated as money because they can be transferred to pay others, even if you never hold physical cash.

Most explanations focus on three core functions, because together they explain why money makes markets work.

Money is the go-between in transactions. Instead of bartering directly (trading one good for another), you can sell something and receive money, then use that money to buy what you need. This reduces the effort needed to find a partner who wants exactly what you have.

A simple scenario: you do freelance work. You want compensation that can be spent broadly—on groceries, transit, rent—not something that only one person will accept. Money’s medium-of-exchange function is what makes that possible.

Money also provides a shared way to express prices. When you see a price tag, a salary offer, or a bank statement balance, those numbers are in money terms. That common measurement makes it easier for people and businesses to compare options and keep track of costs.

Without a unit of account, pricing would require constant negotiation in “equivalents” across different goods. Money turns that into a straightforward number.

Finally, money can be saved for later. If you hold money today, you expect it to help you buy goods later. This function depends on stability—especially stability in purchasing power.

Important boundary: store of value doesn’t mean money never loses value. Inflation can reduce what a fixed amount of money can buy. In that case, money still works for payments, but it’s a less reliable tool for saving.

A common misunderstanding is equating “money” with “wealth” or “anything valuable.” In reality, money is a specific tool defined by how people use it.

Wealth includes many assets: property, stocks, business ownership, collectibles, and more. Some of these can be valuable, but they’re not always accepted as payment in daily life. If an asset is hard to spend quickly or requires a complex conversion step, it doesn’t function as money in the same way.

Another misunderstanding is assuming money is only physical cash. While cash is money, many economies rely heavily on bank deposits and electronic transfers. The economic function matters more than the form.

Economists often talk about different categories of money based on how liquid they are—how quickly you can use them for spending.

You’ll commonly see distinctions like:

You don’t need to memorize these categories to understand the main point: the “money” you can spend immediately is different from assets that might be valuable but aren’t instantly usable.

This is also why the phrase “money 100 dollar bill” is a useful everyday reminder. A single bill is only part of the story. The economic question is whether the currency is widely accepted and stable enough to serve the functions above.

Money’s jobs are visible in ordinary behavior.

When money is doing well as a medium of exchange, you can pay for things without special arrangements. When you can use a card, a bank transfer, or cash interchangeably, that’s a sign the payment system supports broad acceptance.

When money is doing well as a unit of account, prices are comparable and stable enough that budgeting makes sense. Businesses can set prices and households can plan purchases. Even if specific prices change, the overall system still provides a common language.

When money is doing well as a store of value, saving feels reasonable. People hold deposits or cash because they expect it to buy roughly similar things later. When money doesn’t hold value well—often due to inflation—people may spend sooner, demand higher wages, or look for alternatives that better preserve purchasing power.

Money isn’t just about convenience. It’s also about coordination.

If you think about why businesses can operate at scale, a shared unit of account is part of the answer. It lets companies calculate costs, set prices, pay workers, and settle debts with consistent numbers. A stable payment system and a predictable currency reduce uncertainty.

Trust is another major piece. People accept money because they believe others will accept it too, and because they believe the money’s value won’t collapse suddenly. That trust is influenced by institutions, monetary policy, and the broader economic environment.

When trust weakens, money can still be used for payments, but its store-of-value role can deteriorate. That’s when you start seeing behavior shifts: people may shorten their savings horizon, convert money into goods, or demand compensation that keeps up with inflation.

You don’t need a textbook to notice money’s performance. Here are practical signals.

Money is working when:

Money is struggling when:

These aren’t “mystery symptoms.” They’re the real-world reflections of the three core functions. If one function weakens, the economy still runs—but daily life becomes more complicated.

Understanding the functions of money can help you avoid vague financial thinking.

If your goal is short-term spending—like a bill due next month—liquidity is usually more important than maximizing return. Cash and cash-like balances make sense because you need access.

If your goal is medium- to long-term saving—like building an emergency fund over time or planning for a big purchase—purchasing power matters. Inflation can reduce what money can buy, so your plan should account for that.

A practical way to think about it is to match the tool to the job. Money is excellent for exchange and quick planning. It’s only a reliable store of value when inflation is manageable and confidence in the currency is stable.

If you’re ever unsure, start with two questions: “When will I need this money?” and “What could inflation do to my purchasing power by then?” Those questions keep you grounded in the economics of money rather than reacting to noise.

Use these two paths when you want the clearest immediate continuation—one for deeper guidance, one for the broader topic map.

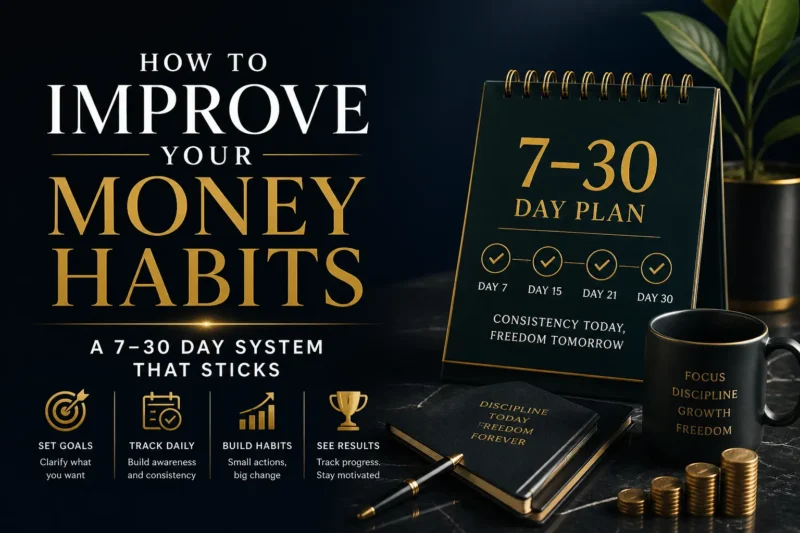

Want better money habits without overwhelm? Try this simple 7–30 day system: track spending, set goals,…

Read nextExplore the broader topic hub for connected guides, references, questions, and works.

Explore topicMost readers do not get stuck because the topic is too complex. They get stuck because they assume one herb, one dose, or one quick answer should solve every situation. In reality, the strongest results usually come from matching the right remedy to the right context and using it with consistency.

When you want broader context around this answer, use these connected pages to expand your understanding across the full cluster.

Want better money habits without overwhelm? Try this simple 7–30 day system: track spending, set goals,…

Read next

Money shapes your daily choices, stress level, and sense of security. Here’s why it matters, what…

Read next

Explore 15 definition of money perspectives, from economics to daily life. Learn what every definition agrees…

Open reference

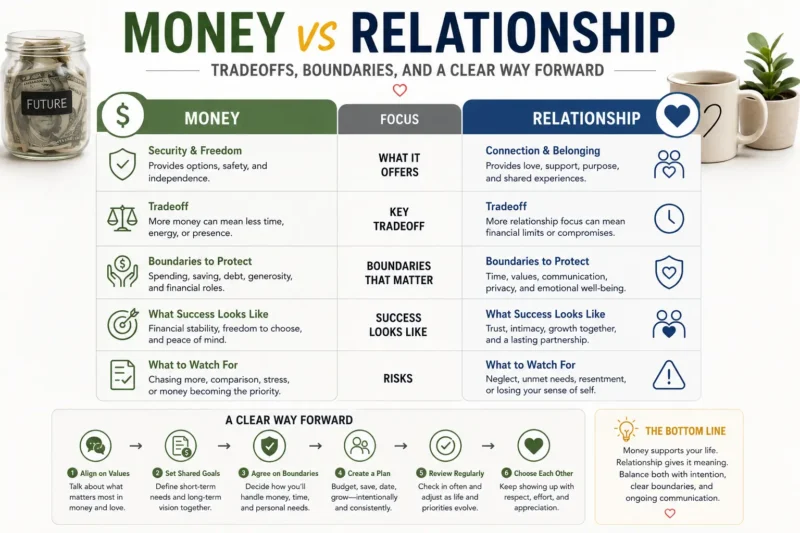

Money vs relationship isn’t a zero-sum choice. Compare the real tradeoffs, spot the conflict triggers, and…

Compare nowNot always. Currency (cash and coins) is a common form of money, but economics defines money by function—broad acceptance for payments and use as a unit of account. In many modern economies, bank deposits and electronic balances function as money even though they aren’t physical notes.

Economists usually describe three functions: money acts as a medium of exchange (it helps you buy and sell), a unit of account (prices and wages are measured in it), and a store of value (you can hold it for later purchases). These functions work best when the currency is stable and trusted.

Yes. Money can remain the medium of exchange even during inflation, because people still need a payment method. However, its store-of-value function weakens when purchasing power falls quickly. In that environment, people may spend faster, demand higher wages, or prefer assets that better track value.

Barter requires a double coincidence of wants: you must find someone who wants what you offer and has what you want. Money breaks that link. You can trade your goods or labor for money, then use that money to buy from someone else, without needing the exact matching partner.

Unit of account means that prices, salaries, and debts are expressed in the same money terms. That shared measurement makes it easier to compare options and plan. Even when you pay digitally, the amounts are still measured in money units, which is why budgeting and accounting stay workable.

In an economy where it’s widely accepted, a 100-dollar bill functions as money because sellers generally take it as payment. The key is acceptance and usability. If a currency loses credibility or becomes hard to spend, even familiar bills may not reliably serve money’s functions.

Money in economics isn’t just “stuff you have.” It’s a shared system that makes exchange easier, prices comparable, and saving possible. When you remember money’s three core jobs, you can better interpret everyday changes—like inflation—without panicking or guessing. Use the concept to choose tools that fit your time horizon: liquidity for near-term needs, and purchasing-power awareness for longer goals.